As specialists in property valuation, we offer professional and reliable assessments of residential, commercial, and industrial properties. Our experienced Valuers provide unbiased and well-researched property valuations that adhere to industry standards and regulations.

Our financial reporting valuations assist businesses in complying with accounting standards and financial reporting requirements. We provide accurate and defensible valuation reports for intangible assets, financial instruments, and other complex valuation scenarios, ensuring compliance with regulatory frameworks and international accounting standards.

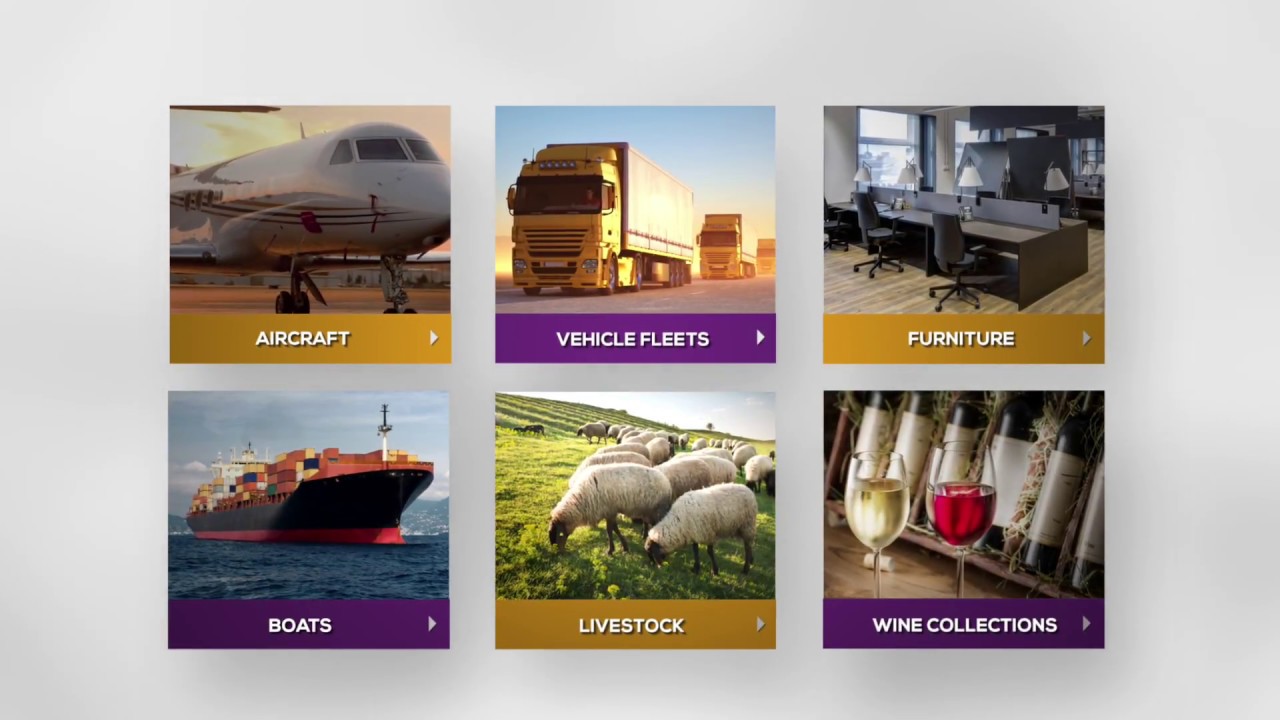

Our asset valuation services encompass a wide range of assets, including machinery, equipment, vehicles, and more. We conduct precise and transparent asset valuations, ensuring you have a clear understanding of your assets' worth for financial reporting, insurance purposes, or asset disposal.

With over 30 years of experience in the Business Sales industry, our expert team of certified business Valuers conducts comprehensive assessments to determine the fair market value of businesses. Whether you are buying, selling, or planning for succession, our accurate and detailed business valuations provide the insights you need to make informed decisions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}